I. Activating Prior Knowledge

We have spent time discussing credit and how it can benefit as well as harm your financial future. Consider some of the reasons why a person might chose to get a credit card. What would be considered strong or good reasons for obtaining a credit card? What would be some weak reasons for obtaining a credit card.

II. Setting A Purpose For Reading

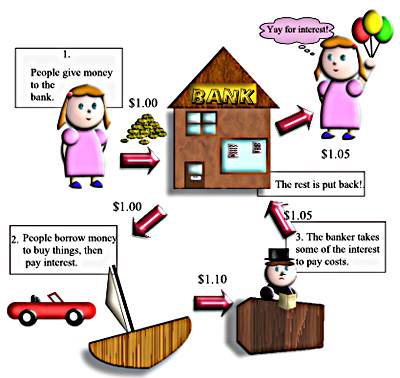

One of the best ways to learn how credit cards work is to actually use one. However, since you are not old enough and do not have a job, it would probably be best to stick with a simulation. In this simulation, you will begin to see how interest accrues on your debt, when you don't pay off the amount on the credit card and how much goods "really" cost when you charge them on a credit card.

III. Read, Read, and Read Again

To begin this simulation, you need to do a little bit of reading about credit cards.

STOP! If you cannot answer these questions, please go back and re-read. What is the difference between a Fixed Annual Percentage Rate (APR) and a Variable APR? What is the difference between a minimum payment and the amount owed? What are some additional fees that a credit card company can charge to their customers?

Now for the simulation:

IV. Personal Reflection

Based on the simulation, answer the following questions in your blog post:

V. Peer Reflection

Select one class mate, whose response has not been evaluated and analyze their responses to the above questions. Provide constructive feedback to their responses.

We have spent time discussing credit and how it can benefit as well as harm your financial future. Consider some of the reasons why a person might chose to get a credit card. What would be considered strong or good reasons for obtaining a credit card? What would be some weak reasons for obtaining a credit card.

II. Setting A Purpose For Reading

One of the best ways to learn how credit cards work is to actually use one. However, since you are not old enough and do not have a job, it would probably be best to stick with a simulation. In this simulation, you will begin to see how interest accrues on your debt, when you don't pay off the amount on the credit card and how much goods "really" cost when you charge them on a credit card.

III. Read, Read, and Read Again

To begin this simulation, you need to do a little bit of reading about credit cards.

STOP! If you cannot answer these questions, please go back and re-read. What is the difference between a Fixed Annual Percentage Rate (APR) and a Variable APR? What is the difference between a minimum payment and the amount owed? What are some additional fees that a credit card company can charge to their customers?

Now for the simulation:

IV. Personal Reflection

Based on the simulation, answer the following questions in your blog post:

- Which card did you select? Why did you chose that particular card?

- Which items did you purchase?

- How much money of the $2,000.00 did you spend?

- What was the minimum payment you were expected to pay?

- How many months would it take to pay for the items, if you only made the minimum payment?

- With interest, what is the total cost of your items that you purchased?

- If you increased the amount you paid, what happened to the time and amount owed? Why did this occur?

- What better methods, if any, could you have employed to obtain these items?

- Why is the wise use of credit cards important?

- Why should you shop around for a credit card? What factors should you consider?

V. Peer Reflection

Select one class mate, whose response has not been evaluated and analyze their responses to the above questions. Provide constructive feedback to their responses.

RSS Feed

RSS Feed