Source: http://library.thinkquest.org/08aug/00196/whatisbank.htm

I. Activating Prior Knowledge

As you have learned, banks offer a variety of services for its customers. Understanding how banks operate is essential for making the best economic decisions for your wallet.

II. Setting A Purpose for Reading

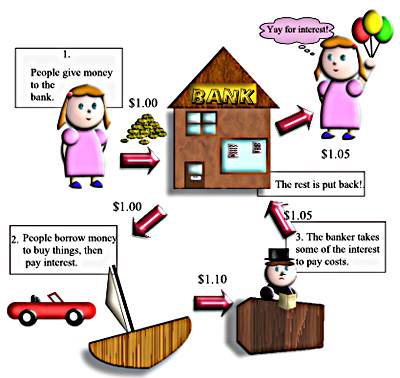

In class, we had an overview of the services that banking provides. This article goes into those services with a little more depth as well as how the money that you deposit into the bank is used to finance additional services. Take a moment to review the diagram. While this is a simplified version of how a bank works, it illustrates the major points.

III. Reading the Text

Banks Are Businesses That Sell Financial Services

Like all privately owned businesses, banks need to earn profits in order to operate. They do this by charging money for the loans, credit cards, checking accounts, and other services they provide.

Where do banks get the money to lend? They get it from their depositors, the people who open accounts. Depositors entrust their money to banks because of the safety they provide, and the interest earned on most accounts. Among other things, the Federal Deposit Insurance Corporation (FDIC) guarantees the safety of bank accounts. The FDIC insures bank accounts in amounts up to $100,000.00

Banks draw upon their depositor’s savings to make loans. Banks pay their depositors interest. Interest earned on savings accounts varies from year to year. Those who borrow pay interest on their loans to the lending banks. Naturally, the interest charged on loans is higher that the interest that banks pay their depositors. The difference between the amount that banks charge for their loans and the amount paid to depositors pays expenses and adds to bank profits. For example a bank may pay 2.5 percent interest on savings accounts while charging 8 percent for car loans.

STOP! See if you can answer the following questions. If not, go back and re-read!

How do banks make money? Define deposit, interest, and loan. How are these terms related to banks making money?

The Federal Reserve System

By now, you may be wondering where the banks get the currency that they give to people who cash checks or use an ATM machine. In 1913, the U.S. Congress created the Federal Reserve System. This agency (often called the “Fed”) operates 12 Federal Reserve Banks in this country. Each of these banks supervises the banking activities in one of the nation’s Federal Reserve districts.

One of the tasks that Congress assigned to the Federal Reserve was to meet the nation’s need for cash. The Fed is able to put currency into the hands of the nation’s banks when they need it, and take it back when they do not need it. Here is how the Fed does this:

A bank maintains an account with the Federal Reserve Bank in its district in much the same way that a person holds an account at a local bank. When a local bank needs cash, it simply withdraws the money from its account at the Fed. When a bank has more cash than it needs, it redeposits the money with the Fed. Sometimes, however, a bank needs more money than it has in its account at the Fed. The bank will then borrow the money it needs from the Fed. The bank will pay interest to the Fed for this borrowed money.

STOP! See if you can answer the following questions. If not, go back and re-read!

What is the purpose of the Federal Reserve System? Does it meet its goal of maintaining the nation’s need for cash?

How Commercial Banks Create Money

Having read this far, perhaps you believe that only the government can create money. This is not the case. A great deal of the money in circulation is created by commercial banks. Commercial banks often make loans to businesses. When a business firm borrows a sum of money, the bank places it on deposit in the firm’s checking account. The business withdraws the money as it needs it.

Take the case of Harry and Sylvia Girard, the owners of the Girard Jewelry Company. In October, they borrowed $15,000.00 from the Safety First National Bank to buy watches and jewelry to sell during the holiday season. The $15,000 was deposited in their checking account at the bank. As the various shipments of merchandise were received, the Girards wrote out check in payment of the bills. After January 1, they repaid the loan with the money they had earned from the sale of the jewelry (plus interest).

In this example, a very interesting event occurred. The country's money supply was increased by $15,000 for a short time, and the government had nothing to do with it. This money was not taken away from anyone - therefore, the bank created $15,000. Commercial banks all over the country do this every day: They create checkbook money by granting loans. Of course, as loans are repaid, money is taken out of circulation. Thus, the Girard's checking account balance was reduced by $15,000 when they repaid their loan.

Since banks earn profits by lending money, it follows that the more they have to lend, the greater their profits will be.

“Now, wait a minute,” you say. “Do you mean to tell me that the bank will take the money I deposited for safekeeping and lend it to someone I don’t even know?”

That is correct. Of course, before it makes a loan the bank does what it can to determine that the business or individual who borrows will be able to pay the money back.

“But how will I and others like me be able to get our money back when we want it if the bank has loaned it out?”

That is easy. Although on any given day some depositors will make withdrawals, other depositors will make deposits. In fact, on most days the amount of deposits will more than offset withdrawals. Furthermore, banks cannot lend all the money they have on deposit. They must always keep part of this amount on hand in case there is a heavy run of withdrawals at a particular time. The sum kept on hand is known as the bank’s reserves. The portion of their total deposits that they must keep on reserve at any one time is determined by the Federal Reserve Board.

Suppose that a bank has $1 million in deposits, and the federal government has said that all banks must keep 20 percent of their deposits on hand as a reserve. How much of its $1 million in deposits could the bank lend out? If you said $800,000 you were absolutely right. The reason is that 20 percent of $1 million is $200,000. This amount must be set aside in the bank’s reserves. The balance of the $1 million, or $800,000, may be given out in loans. But the process does not stop there. If the full $800,000 loaned out is redeposited and the bank keeps 20 percent $160,000 as a reserve, $640,000 can be loaned out.

There is a limit to the amount of money a bank may create because there is a limit to the amount of money it may lend. Remember, a bank must keep some money – reserves – on hand to meet the demands of its depositors.

Source: Antell, G. and Harris, W. Economics for Everybody. NY: Amsco, Inc. 2007. p. 74-81.

STOP! See if you can answer the following questions. If not, go back and re-read!

Summarize, in your own words, how banks make money? What happens to the system when someone does not repay the debt or loan obligation?

IV. Personal Reflection

1. Should banks loan money that you deposit to other people? Explain your response.

2. How does the federal reserve protect the interest of citizens? Explain your response.

3. What happens to the system when a borrower does not repay their loan or default on the debt?

V. Peer Reflection

1. Read one classmate’s response to question. Analyze their response. Do you agree or disagree? Why or why not?

I. Activating Prior Knowledge

As you have learned, banks offer a variety of services for its customers. Understanding how banks operate is essential for making the best economic decisions for your wallet.

II. Setting A Purpose for Reading

In class, we had an overview of the services that banking provides. This article goes into those services with a little more depth as well as how the money that you deposit into the bank is used to finance additional services. Take a moment to review the diagram. While this is a simplified version of how a bank works, it illustrates the major points.

III. Reading the Text

Banks Are Businesses That Sell Financial Services

Like all privately owned businesses, banks need to earn profits in order to operate. They do this by charging money for the loans, credit cards, checking accounts, and other services they provide.

Where do banks get the money to lend? They get it from their depositors, the people who open accounts. Depositors entrust their money to banks because of the safety they provide, and the interest earned on most accounts. Among other things, the Federal Deposit Insurance Corporation (FDIC) guarantees the safety of bank accounts. The FDIC insures bank accounts in amounts up to $100,000.00

Banks draw upon their depositor’s savings to make loans. Banks pay their depositors interest. Interest earned on savings accounts varies from year to year. Those who borrow pay interest on their loans to the lending banks. Naturally, the interest charged on loans is higher that the interest that banks pay their depositors. The difference between the amount that banks charge for their loans and the amount paid to depositors pays expenses and adds to bank profits. For example a bank may pay 2.5 percent interest on savings accounts while charging 8 percent for car loans.

STOP! See if you can answer the following questions. If not, go back and re-read!

How do banks make money? Define deposit, interest, and loan. How are these terms related to banks making money?

The Federal Reserve System

By now, you may be wondering where the banks get the currency that they give to people who cash checks or use an ATM machine. In 1913, the U.S. Congress created the Federal Reserve System. This agency (often called the “Fed”) operates 12 Federal Reserve Banks in this country. Each of these banks supervises the banking activities in one of the nation’s Federal Reserve districts.

One of the tasks that Congress assigned to the Federal Reserve was to meet the nation’s need for cash. The Fed is able to put currency into the hands of the nation’s banks when they need it, and take it back when they do not need it. Here is how the Fed does this:

A bank maintains an account with the Federal Reserve Bank in its district in much the same way that a person holds an account at a local bank. When a local bank needs cash, it simply withdraws the money from its account at the Fed. When a bank has more cash than it needs, it redeposits the money with the Fed. Sometimes, however, a bank needs more money than it has in its account at the Fed. The bank will then borrow the money it needs from the Fed. The bank will pay interest to the Fed for this borrowed money.

STOP! See if you can answer the following questions. If not, go back and re-read!

What is the purpose of the Federal Reserve System? Does it meet its goal of maintaining the nation’s need for cash?

How Commercial Banks Create Money

Having read this far, perhaps you believe that only the government can create money. This is not the case. A great deal of the money in circulation is created by commercial banks. Commercial banks often make loans to businesses. When a business firm borrows a sum of money, the bank places it on deposit in the firm’s checking account. The business withdraws the money as it needs it.

Take the case of Harry and Sylvia Girard, the owners of the Girard Jewelry Company. In October, they borrowed $15,000.00 from the Safety First National Bank to buy watches and jewelry to sell during the holiday season. The $15,000 was deposited in their checking account at the bank. As the various shipments of merchandise were received, the Girards wrote out check in payment of the bills. After January 1, they repaid the loan with the money they had earned from the sale of the jewelry (plus interest).

In this example, a very interesting event occurred. The country's money supply was increased by $15,000 for a short time, and the government had nothing to do with it. This money was not taken away from anyone - therefore, the bank created $15,000. Commercial banks all over the country do this every day: They create checkbook money by granting loans. Of course, as loans are repaid, money is taken out of circulation. Thus, the Girard's checking account balance was reduced by $15,000 when they repaid their loan.

Since banks earn profits by lending money, it follows that the more they have to lend, the greater their profits will be.

“Now, wait a minute,” you say. “Do you mean to tell me that the bank will take the money I deposited for safekeeping and lend it to someone I don’t even know?”

That is correct. Of course, before it makes a loan the bank does what it can to determine that the business or individual who borrows will be able to pay the money back.

“But how will I and others like me be able to get our money back when we want it if the bank has loaned it out?”

That is easy. Although on any given day some depositors will make withdrawals, other depositors will make deposits. In fact, on most days the amount of deposits will more than offset withdrawals. Furthermore, banks cannot lend all the money they have on deposit. They must always keep part of this amount on hand in case there is a heavy run of withdrawals at a particular time. The sum kept on hand is known as the bank’s reserves. The portion of their total deposits that they must keep on reserve at any one time is determined by the Federal Reserve Board.

Suppose that a bank has $1 million in deposits, and the federal government has said that all banks must keep 20 percent of their deposits on hand as a reserve. How much of its $1 million in deposits could the bank lend out? If you said $800,000 you were absolutely right. The reason is that 20 percent of $1 million is $200,000. This amount must be set aside in the bank’s reserves. The balance of the $1 million, or $800,000, may be given out in loans. But the process does not stop there. If the full $800,000 loaned out is redeposited and the bank keeps 20 percent $160,000 as a reserve, $640,000 can be loaned out.

There is a limit to the amount of money a bank may create because there is a limit to the amount of money it may lend. Remember, a bank must keep some money – reserves – on hand to meet the demands of its depositors.

Source: Antell, G. and Harris, W. Economics for Everybody. NY: Amsco, Inc. 2007. p. 74-81.

STOP! See if you can answer the following questions. If not, go back and re-read!

Summarize, in your own words, how banks make money? What happens to the system when someone does not repay the debt or loan obligation?

IV. Personal Reflection

1. Should banks loan money that you deposit to other people? Explain your response.

2. How does the federal reserve protect the interest of citizens? Explain your response.

3. What happens to the system when a borrower does not repay their loan or default on the debt?

V. Peer Reflection

1. Read one classmate’s response to question. Analyze their response. Do you agree or disagree? Why or why not?

RSS Feed

RSS Feed